Kindly Note:

- This blog post is made from the video shared by Markets by Zerodha, and the summary is for easy reference for people who are unable to watch a 28+ minute video.

- Companies mentioned are not stock recommendations.

Introduction

India’s plastic pipe sector is currently witnessing a massive transformation. While the industry is already worth several hundred crores, it is projected to grow at a 12% CAGR through FY27 [00:08]. With India consuming approximately 369 crore kg of plastic pipes annually, a number expected to hit 562 crore kg by FY30, major industry players like Supreme Industries, Astral, Finolex, and Prince Pipes are committing thousands of crores in Capex to meet the upcoming demand [00:22].

1. From Iron to Plastic: A Brief History

The story of pipes in India began in 1968. Initially, the market was dominated by Galvanized Iron (GI) pipes. While strong, they were heavy and prone to rusting, requiring expensive replacements every 15–20 years [01:57].

The first plastic experiment with uPVC in the 1970s failed because manufacturers incorrectly mixed uPVC with GI, leading to cracks and leaks in India’s heat [02:43]. However, this failure paved the way for high-quality, long-lasting plastic pipes that returned in the early 2000s and now dominate the market.

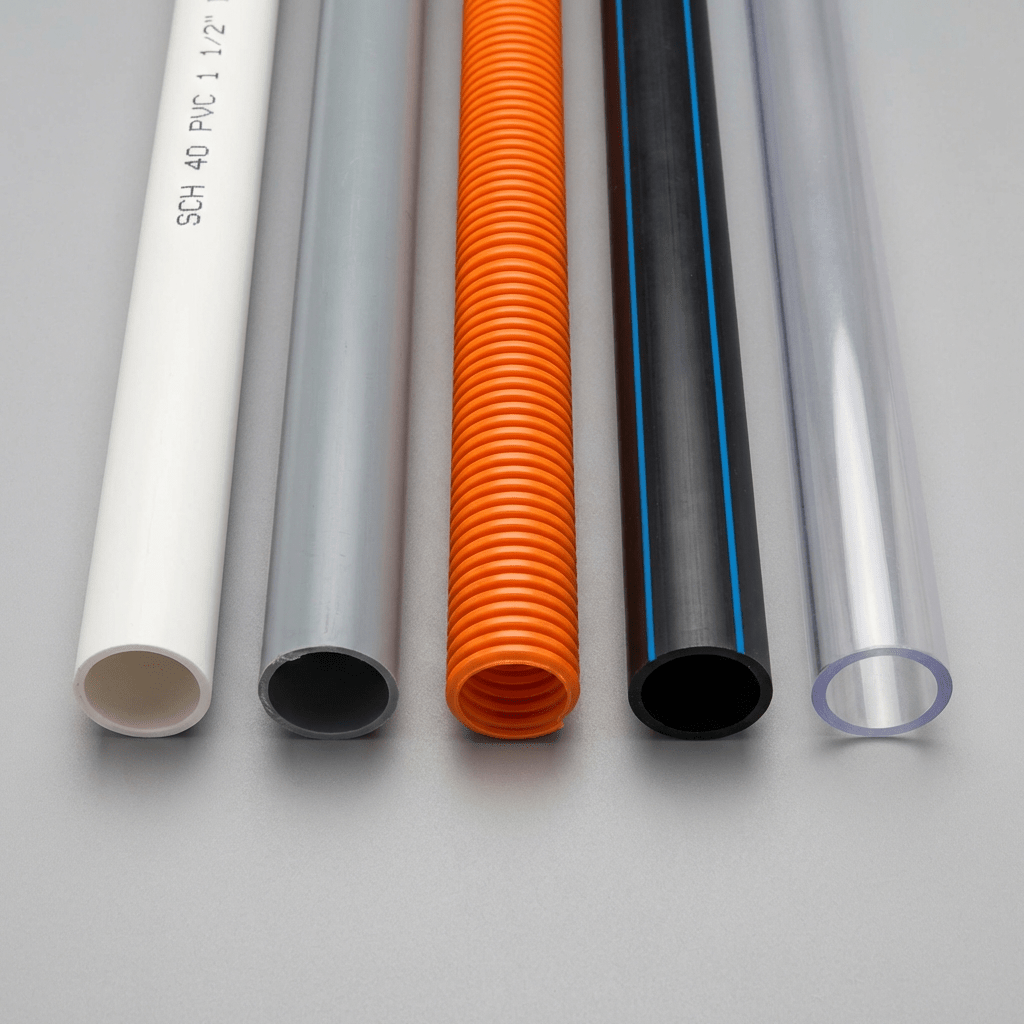

2. The Five Major Types of Plastic Pipes

Understanding the “Product Mix” is crucial for investors, as different pipes have different temperature tolerances and profit margins:

- uPVC (Unplasticized PVC): The most affordable and common (65% market share). Used for cold water, irrigation, and drainage [05:43].

- cPVC (Chlorinated PVC): An upgraded version that can handle hot water up to 93°C. It is the gold standard for residential plumbing [03:43].

- HDPE (High-Density Polyethylene): Flexible and extremely durable (50–100 years). Primarily used for main water lines, gas distribution, and industrial plants [04:27].

- oPVC (Oriented PVC): A newer category replacing iron pipes in large government water supply projects due to its high-pressure tolerance [04:57].

- PPR (Polypropylene Random): The most premium segment. While currently only 5% of the Indian market, it is growing fast in luxury housing [05:19].

3. The Chemistry and Cost of Manufacturing

Every plastic pipe starts with Crude Oil (Ethylene) and Salt (Chlorine) [06:50]. These are combined to form PVC Resin, a white powder that is the primary raw material.

- Import Dependency: India produces only 18 lakh metric tons of PVC resin but demands 47 lakh metric tons, forcing us to import 62% of our requirement from China, South Korea, and the USA [07:46].

- Cost Drivers: Raw materials account for 65–70% of the total cost [08:52]. Consequently, fluctuations in global crude oil prices or “dumping” of cheap resin by China directly impact the profit margins of Indian companies [19:01].

4. Four Structural Drivers Powering Growth

Why are companies like Supreme Industries announcing a CapEx of ₹1,200 crore for FY26? The demand is coming from four main areas:

- Agriculture: Only 52% of India’s cultivated land is irrigated. Government schemes like Pradhan Mantri Krishi Sinchai Yojana are driving massive demand for irrigation pipes [11:28].

- Infrastructure Capex: Projects such as the Jal Jeevan Mission, Swachh Bharat, and Smart Cities require extensive piping networks [11:53].

- Real Estate & “Prizmization”: The shift toward premium, larger homes (1,600+ sq. ft.) means more bathrooms and plumbing, driving demand for high-margin cPVC pipes [12:43].

- Replacement Demand: Roughly 35% of current demand comes from replacing old, rusted iron pipes with modern plastic alternatives [13:46].

5. Key Indian Players & Their Strategies

The organized sector holds about 60–65% of the market share, led by four giants:

| Company | Key Strategy | Performance Note |

| Supreme Industries | Market leader with 14,500+ SKUs. Shifting focus from Agri (low margin) to cPVC (high margin) [16:57]. | Strongest revenue per dealer [23:15]. |

| Astral Pipes | The pioneer of cPVC in India. High residential focus (80%) and industry-leading EBITDA margins (~17%) [16:11]. | Largest distribution network with 2.5 lakh dealers [23:07]. |

| Finolex Industries | The only player with Backward Integration, making its own PVC resin [21:23]. | Leader in the uPVC agriculture segment [18:14]. |

| Prince Pipes | Building capacity in cPVC and expanding into sanitaryware (Acquired Aquel) to leverage its distribution network [18:01]. | Growing its market share through government project orders [18:08]. |

6. Risks to Watch Out For

- Over-Supply: Most companies are currently operating at below 60% capacity utilization, yet they continue to expand. If demand stalls, excess capacity could lead to price wars [25:48].

- Falling cPVC Premiums: As more players enter the cPVC segment, the price gap between uPVC and cPVC is narrowing, which may shrink future margins [26:15].

- Global Volatility: High reliance on imported resin makes the sector vulnerable to geopolitical tensions and shipping costs [22:26].

Conclusion

India’s plastic pipe industry is no longer just a “commodity” business. By focusing on Backward Integration (making their own resin) and Product Mix (shifting to premium PPR and cPVC), Indian companies are preparing for a decade of infrastructure growth. If the real estate and agriculture boom continues, the “Great Indian Pipe Race” is only just beginning.

PS: This blog post is based on the research by Markets by Zerodha for easy referral.

Watch the full video here:

Leave a comment