Background

Ambuja Cements Ltd, a part of the global conglomerate LafargeHolcim, is among the leading cement companies in India[11]. It currently has a capacity of 29.65 million tonnes with five integrated cement manufacturing plants and eight cement grinding units across the country.

Fig 1. Logo of Ambuja Cement

The company has many firsts to its credit – a captive port with four terminals that has facilitated timely, cost-effective, cleaner shipments of bulk cement to its customers.

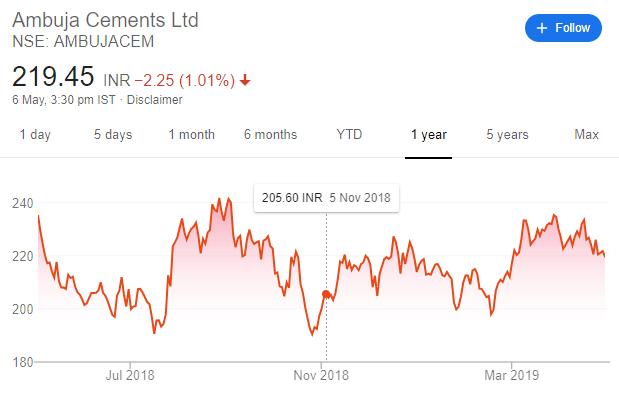

Ambuja Cement Stock Performance

Graph 1: Ambuja Cement Stock (NSE) [17]

1-year return: ~ -6 to -7%

Some Reasons for Dismal Return[13]

- Excess cement capacity: Cement industry has been experiencing glut situation as there has been a mammoth mismatch between cement demand and its supply

- Acute shortage of coal: Coal is one of the major raw materials needed by the industry both in the manufacturing of cement and also for generating power. The situation got much grimmer when the Supreme Court banned the usage of petcoke in Aug 2018[15]

- High Operating Cost: Fuel, Coal, and Transportation

Graph 2: Cement Industry Expenses Split [13]

Initiatives[11]

Ambuja is adding capacity in Central & East India where the government intends to spend on railways and ports[5]. Ambuja gives a very unique opportunity of brand value and product portfolio. Currently, it is trying very hard to improve capacity utilization and operating margin.

Concurrently, it is trying to circumvent the current commodity onslaught by introducing new products like Ambuja Plus Roof Special, Ambuja Plus Cool Walls and Ambuja Compocem which come under the category of Green Building solutions to reduce the carbon footprint[6].

Industry Tailwinds[16]

- Operational efficiency due to lower freight cost and power consumption

- Rupee Appreciation

- Lower Petcoke & Coal prices

Financials

Fig 2. Ambuja Cement(in red) performance over the years[10]

The financials of the company are as follows[1][2][3][4]

– The stock is currently trading around Rs. 218-222

– Face Value Rs. 2

– Book value Rs. 139.01

– Price/Earning = 19.1

– Return = -5.76%(Raw Material Cost & Pet Coke Ban of Supreme Court)[8][9]

– 200 Day Moving Average (DMA) – Rs 217.61

– Dividend yield (0.68%)

– Price/Book= 1.58

Overall View:

The distribution network and brand equity can go a long way if the company is able to surpass the storm which is lashing the cement industry in the short term.

With the focus on infrastructure in the coming years, it can turn out to be a dark horse.

PS: This is just a stock review not a recommendation

If you want to share your opinion kindly do so in the comments section or email me at u2d2tech@gmail.com

References

- https://www.valueresearchonline.com/stocks/snapshot.asp?code=1374

- https://www.moneycontrol.com/india/stockpricequote/cement-major/ambujacements/AC18

- https://www.indiainfoline.com/company/ambuja-cements-ltd/quote/218

- https://www.moneycontrol.com/financials/ambujacements/ratios/AC18

- https://www.bloombergquint.com/business/acc-ambuja-cements-signal-stress-slowdown-in-annual-reports

- https://www.worldcement.com/indian-subcontinent/02042019/ambuja-cement-launches-ambuja-plus-cool-walls/

- https://www.indiainfoline.com/article/equity-earnings-result-commentary/ambuja-cements-ltd-quarterly-results-ambuja-cements-ltd-s-q3fy19-standalone-net-profit-declines-36-61-yoy-to-rs214-50cr-misses-estimates-119021900246_1.html

- https://www.thehindubusinessline.com/markets/commodities/india-bans-pet-coke-import-for-use-as-fuel/article24716341.ece

- https://www.livemint.com/Politics/QMz7m5wPxmNjIvrsCFR0LI/Government-bans-petcoke-import-for-use-as-fuel.html

- https://www.valueresearchonline.com/stocks/snapshot.asp?code=1374

- https://www.ambujacement.com/about-ambuja/ambuja-at-a-glance

- https://www.indiamart.com/proddetail/ambuja-cement-10207910648.html

- http://www.indiancementreview.com/News.aspx?nId=3Eu6Z0tx/25lzM6ruCDnjg==

- https://www.livemint.com/Money/iZjwRtKGHLyZCP6JS7DLOM/The-cement-industrys-problem-of-plenty.html

- https://www.thehindubusinessline.com/markets/commodities/india-bans-pet-coke-import-for-use-as-fuel/article24716341.ece

- https://www.bloombergquint.com/bq-blue-exclusive/what-fuelled-the-latest-cement-stock-rally

- https://www.google.com/search?ei=jX3QXM_xIZP0rQGylIX4Cg&q=ambuja+cement+share&oq=Ambuja+Cen&gs_l=psy-ab.1.3.0i10l10.621767.623858..626995…0.0..0.547.2441.0j4j4j1j0j1……0….1..gws-wiz…….0i71j35i39j0i67j0i131i67j0i131j0.KXFuzuRBVZk

Like!! I blog quite often and I genuinely thank you for your information. The article has truly peaked my interest.

LikeLiked by 1 person

I like the efforts you have put in this, appreciate it for all the great articles.

LikeLike

You actually make it appear so easy along with your presentation however I find this topic to

be actually something that I think I might by no means understand.

It sort of feels too complex and very large for me.

I’m having a look forward to your subsequent publish, I will attempt to get the hang of it!

LikeLike

I am sure this post has touched all the internet people, its really

really fastidious piece of writing on building up new webpage.

LikeLike

What i don’t understood is in reality how you are

now not actually much more neatly-favored than you may be right now.

You are very intelligent. You know thus significantly relating

to this topic, made me in my view believe it

from so many various angles. Its like men and women don’t seem to be fascinated except

it is one thing to do with Girl gaga! Your individual stuffs great.

All the time take care of it up!

LikeLike

It’s awesome designed for me to have a website, which is useful

in favor of my know-how. thanks admin

LikeLike